Everton Financial Results 2024/25

- Matchday Finance

- Apr 3

- 17 min read

The 2024/25 season was Everton’s 71st consecutive year in the Premier League and their final season at Goodison Park.

The campaign was one of significant change at this historic club. In addition to the final season at Goodison Park after 133 years at the ground, the club also underwent a change of ownership, bringing an end to Farhad Moshiri’s seven-year tenure.

On the pitch, Everton sat 16th in the table midway through the season, just above the relegation places. This prompted the club to replace manager Sean Dyche with David Moyes, who returned for a second spell in charge. Moyes quickly steadied the side, guiding them to safety with a 10-match unbeaten run, and the club ultimately finished in 13th place on 48 points.

The club was acquired by the Friedkin Group in December 2024, when they purchased Farhad Moshiri’s 94% stake, making Everton the 10th Premier League club under American ownership. This brought an end to a difficult period in which, despite Moshiri investing around £750 million, there were ongoing concerns over the club’s financial stability and the risk of administration.

This season is their first at the new Hill Dickinson Stadium and the first full campaign under the new owners. Whilst the new stadium has yet to become the fortress they hoped for, strong away form has lifted the club to 8th place, just three points outside the Champions League positions. After three years of relegation battles, points deductions, failed takeovers and spiralling debt, it is fair to say this is a better position than many would have hoped.

The recent financial challenges has constrained investment in the squad, with Everton recording one of the lowest levels of player acquisitions in the league and the lowest squad book value. In this context, David Moyes has clearly done an excellent job, once again demonstrating his ability to build a competitive, well-organised team on a limited budget.

Everton Financial Results 2024/25

Everton increased revenue by £10 million to £197 million. However, with staff costs exceeding revenue, the club continued to generate operating losses. These were offset by £31 million in player trading profits and one-off asset sales of the women’s team and Goodison Park Limited, which produced a £49 million gain on disposal. As a result, the club reported a £9 million loss; excluding the asset sale gain, the underlying loss would have been £58 million.

Financial highlights:

Revenue: Total revenue reached £197 million, up £10 million year-on-year, driven primarily by higher commercial income.

Staff costs: Wages fell by £4 million (the fourth consecutive annual reduction) to £152 million, likely the 16th highest in the league. Total staff costs were £203 million, equivalent to 103% of revenue, broadly in line with other non–Big Six clubs.

Player sales: The club generated £31 million from player sales, mainly from the sale of Amadou Onana to Aston Villa.

Profit/loss: Everton reported a £9 million loss, supported by a £49 million gain on the sale of the women’s team and Goodison Park Limited. Excluding these disposals, the underlying loss was £58 million.

Net assets: Net assets increased to £393 million, reflecting the debt restructuring as part of the takeover and a further £114 million invested in the new stadium.

Player trading: Everton spent £52 million on new signings, including Jake O’Brien, Iliman Ndiaye, and Carlos Alcaraz. This was more than offset by £56 million in player sales.

Loans and debt: Total debt fell from over £1 billion to £469 million after a £450 million shareholder loan to the previous owner was converted into equity. External borrowings were also refinanced, with the majority now structured over a 30-year term.

Cash Flow: The club recorded operating cash inflows of £2 million and net investment outflows of £37 million, funded by a net increase in loans of £87 million.

Financial Outlook

Everton are clearly entering a new era, defined by a new stadium, new ownership, and a more stable financial foundation. While many supporters understandably felt a sense of loss leaving Goodison Park, the fan experience at the Hill Dickinson Stadium has been largely positive. The decision to bring back David Moyes for a second spell also appears to have been a masterstroke—he has steadied the ship, avoided what could have been a disastrous relegation, and could guide the club to a top-half finish and a possible European place.

Financially, the club is on a much firmer footing, largely due to the £450 million loan write-off as part of the takeover and the restructuring of previously expensive short-term debt. However, whilst staff costs have been reduced, the club remains loss-making, with operating expenses still exceeding revenue. In the latest accounts, Everton would have reported a £58 million loss were it not for the sale of the women’s team and Goodison Park Limited.

Looking ahead, the financial picture is set to evolve. The new stadium should significantly boost matchday and commercial revenues, while an improvement on a 13th-place finish would further increase Premier League distributions, on top of the uplift from a new broadcast cycle. Current estimates suggest revenue could rise to around £250 million, although costs are also expected to increase. With limited player sales recorded so far this season, the club is still likely to post a loss, with our estimates in the region of £20–50 million.

This also marks the final year under the current Profit and Sustainability Rules, which Everton have breached in the past. Assuming last season’s asset sales are deemed allowable by the Premier League (as was the case with Chelsea), the club’s three-year adjusted losses should fall within the permitted limits. They also appear well positioned to comply with the new Squad Cost Ratio set to come into effect next year.

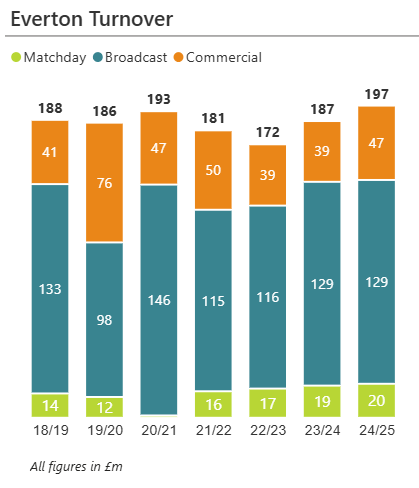

Turnover

Revenue is generated from three primary streams: matchday income (ticket sales), broadcasting distributions (from the Premier League and, where applicable, UEFA competitions), and commercial activities, including sponsorships, merchandising, and other business operations.

The club has experienced limited revenue growth across all streams over the past eight seasons. However, in their final season at Goodison Park, total revenue rose slightly to £197 million, up from £187 million in the prior year.

Everton's revenue will likely ranked 12th in the league.

Matchday Revenue

Matchday revenue is driven by several factors, including the number of home fixtures, average attendance, ticket pricing, hospitality and premium seating. Domestic cup competitions are an exception, as gate receipts are shared between the participating clubs and the FA.

The 2024/25 season was Everton’s final campaign at Goodison Park, which had been their home since 1892. Goodison was a traditional English ground, tightly packed into a residential area with stands close to the pitch. While this helped create an intense atmosphere, it was not well suited to the demands of a modern football club. With a capacity of just under 40,000 and limited scope for expansion, its aging facilities constrained matchday income and broader commercial revenue growth.

During this final season at Goodison, the club averaged 39,173 fans per league match, a slight increase on the previous year. However, the club participated in three fewer domestic cup fixtures, where revenue is shared, leading to a small 3% decline in total attendance to 811,000.

Historically, Everton have maintained relatively low ticket prices. In their final season at Goodison, only a modest increase was applied to adult season tickets, while concession prices remained unchanged. As a result, average revenue per fan rose to £25.03, up from £22.93 the previous season. Despite this increase, it remained one of the lowest yields per fan in the league, broadly comparable with Bournemouth and behind clubs such as Nottingham Forest and Aston Villa.

The combination of higher prices and a slight increase in league attendances contributed to a rise in matchday revenue from £19.1 million to £20.3 million.

Everton's matchday revenue ranks 14th in the league.

The club had been searching for a its new home for several years, with the Bramley-Moore Dock site identified as part of a wider regeneration of the area. Plans for the new stadium were approved in February 2001. The first competitive match held at the new stadium saw Everton host Brighton on 24 August 2025.

There is expected to be a marked increase in matchday revenue following the move to the Hill Dickinson Stadium. The additional capacity, combined with a higher yield per fan, is projected to increase matchday revenues by approximately £10–15 million.

Broadcast Revenue

Broadcast revenue is generated primarily through central Premier League distributions, UEFA payments from European competitions and the club’s own media activities.

The 2024/25 season marked the third and final year of the Premier League’s current broadcast cycle, with total distributions broadly consistent with 2023/24 levels. Approximately 67% of broadcast income is shared equally among clubs, with the remainder allocated through merit payments based on league position and facility fees linked to the number of live televised matches.

Everton’s 13th-place finish earned them £132 million in central distributions, unchanged from the previous season, as the higher league position (and associated merit payments) was offset by fewer televised matches (16 compared to 23).

The chart below shows club-by-club distributions published by the Premier League, with each league position worth close to £3 million in merit payments.

Everton last participated in European competition in the 2014/15 season. While European qualification may have been beyond the expectations of many fans following recent relegation battles, the possibility still remains. At the time of this report, they are only three points behind city rivals Liverpool, who occupy fifth place, a position that is likely to secure a Champions League spot this season. Qualification for Europe would represent an outstanding achievement, particularly given that the club’s squad investment has been severely limited in recent seasons due to financial constraints.

For reference, the chart below shows combined broadcast revenue, including Premier League distributions, UEFA payments, and income from the recently expanded FIFA Club World Cup, which was contested only by Chelsea and Manchester City.

Commercial Revenue

Everton’s sponsorship, advertising and merchandising revenue totalled £24.3 million, an increase of £2.7 million on the prior year. This growth was driven by uplifts on existing sponsorship renewals and the addition of new commercial partners, including Red Bull, Nemiroff and Corpay.

Like many Premier League clubs, Everton have partnered with the betting industry, with casino and sports betting platform Stake.com serving as front-of-shirt sponsor. The deal, reportedly worth £10–12 million per year, was structured as a two-year agreement ahead of the ban on gambling sponsorship on club kits from the 2026/27 season. The partnership attracted some controversy, as Stake no longer holds a UK licence. Other key partners include British watch brand Christopher Ward and kit supplier Castore.

Other commercial revenue amounted to £22.9 million, up £5.9 million year-on-year. This increase was partly driven by revenue linked to the new stadium, including Everton Way stones, as well as commemorative Goodison Park leaving packages and seat sales.

It is also worth noting that the club outsources its retail operations, meaning it does not recognise the full retail income in its accounts. The club has stated that, if it operated retail in-house, this would add approximately £10 million to reported revenue. However, costs would also increase accordingly under such a model.

As the chart below illustrates, the “Big Six” remain on a distinctly higher scale for commercial revenue, although Newcastle United and Aston Villa have experienced significant growth following recent Champions League participation. Everton's commercial revenue rank 11th in the league.

Staff Costs

Staff costs comprise salaries and wages for all employees, the amortisation of transfer fees (the allocation of a player’s acquisition cost over the length of their contract), and impairment charges. Impairments arise when a player’s estimated recoverable value falls below their carrying value on the balance sheet.

Everton’s high staff costs have been a major factor in their financial difficulties. Between 2019 and 2021, staff costs (comprising salaries and amortisation) were running at around 150% of revenue. Since then, and following Premier League sanctions, staff costs have been gradually reduced.

Salaries and wages have declined in each of the past four years, albeit modestly, falling again last season from £157 million to £152 million. Amortisation, however, has seen a more pronounced reduction. With the club restricting investment in new players—among the lowest in the league over the past three seasons—amortisation has decreased and is now close to half of what it was in 2020.

Everton’s total staff costs are likely to rank 16th highest in the league and likely only a third of highest spending club Chelsea (note several clubs are yet to publish staff cost details). With a 13th place finish, the club therefore outperformed relative to its staff cost base.

Everton’s total staff costs of £202 million equate to 103% of revenue, which is below the Premier League average and among the lowest outside the “Big Six.” This represents a positive development for the club. Although they have endured two challenging seasons on the pitch, their performance this season appears to be outperforming their staff cost ranking.

Profit on Player Sales

Player sales have been an important source of income for Everton over the past few seasons, helping to offset high staff costs relative to revenue and reduce overall losses. Notable profitable transfers in recent years include Anthony Gordon’s move to Newcastle United and Richarlison’s transfer to Tottenham Hotspur.

In 2024/25, the club generated £31 million in profits, primarily from the sale of Amadou Onana to Aston Villa and, to a lesser extent, Neal Maupay’s move to Marseille.

Among the clubs that have published full financial results to date, Everton's profit from player sales ranks 8th highest.

Based on sales to date, the club is expected to generate limited profit this season, with Youssef Chermiti’s transfer to Rangers for £7 million representing the only significant departure.

Squad Cost Ratio

The Premier League will implement a new set of financial rules from the 2026/27 season, replacing the existing Profitability and Sustainability Rules (PSR). A central metric under the new framework is the Squad Cost Ratio, which caps clubs’ on-pitch spending at 85% of football-related revenue, including net profit or loss from player sales (based on the average over the last three seasons).

This metric is broadly aligned with UEFA’s Squad Cost Ratio, which is set at a stricter 70%. As a result, clubs not competing in European competitions can invest at relatively higher levels than those, like Liverpool, already active in Europe.

Based on our estimates, Everton’s squad cost ratio is around 69%, assuming that “football-only” wages account for 75% of total salaries and wages. This is well within the current limits, and would also remain compliant under UEFA’s stricter thresholds should the club qualify for European competition.

Profit and Loss

Everton’s PSR breach followed several years of significant losses under previous owner Farhad Moshiri. In the three years to the end of the 2020/21 season, the club recorded cumulative losses of £373 million. Given that the club was also preparing to embark on an £800 million stadium project at the time, it is unsurprising that financial pressures emerged.

The combination of these historic losses and the substantial capital required for the stadium has placed constraints on the club’s finances. As noted, Everton have reduced wage costs and operated with one of the lowest player acquisition budgets in the league. While these measures have helped bring costs down, the club remains loss-making. Revenue growth has been limited in recent seasons, and day-to-day operating expenses continue to exceed income.

With PSR rules still in force for 2024/25 and the current season, the club took steps to improve its financial position by selling its women’s team, following a similar approach previously used by Chelsea and Aston Villa, as well as selling Goodison Park Stadium Limited. Both transactions were carried out by Everton Football Club Company Limited to its parent company, Roundhouse Capital Holdings. While these assets remain under the control of the Friedkin Group, the transactions enabled the club to recognise a combined profit of £49.2 million.

Whilst PSR is on its way out, it remains questionable to many as to why these 'accounting' transactions are allowable against PSR targets.

In 2024/25, Everton’s total revenue reached £197 million, an increase of £10 million year-on-year. Wage costs fell by £4 million, although other operating expenses increased by £11 million as the club prepared for the move to the new stadium. As a result, EBITDA (earnings before interest, tax, depreciation, and amortisation) improved by £21 million to negative £11 million. This marks the seventh consecutive season in which the club has reported negative EBITDA.

After accounting for £51 million in player amortisation and £3 million in depreciation, the club recorded an operating loss of £64 million. While this figure appears substantial, very few Premier League clubs report an operating profit, and the loss is broadly in line with the league average.

The operating deficit was offset by £31 million in profit from player sales and £49 million from the combined sale of the women’s team and Goodison Park Limited. The club also incurred £11 million in exceptional costs relating to payments to former employees, alongside £13 million in interest expenses. This resulted in a net loss of £8.6 million. Excluding the asset sales of the women’s team and Goodison Park Limited, the loss would have been approximately £58 million.

All clubs except Southampton have now reported their profit figures. Chelsea recorded the largest loss at £262 million, the biggest ever reported in the Premier League. Six clubs reported a profit, with the total losses across the league amounting to £796 million.

However, several clubs (including Everton) recorded one-off asset sales in 2024/25. Newcastle reported a £133 million gain on the sale of Newcastle United Projects Limited and St James’ Park leasehold improvements to another group entity. Aston Villa sold their women’s team to a group entity, with the final figure yet to be disclosed but potentially as high as £100 million. Everton also recorded a £49 million gain from the sale of their women’s team and Goodison Park Limited to a group entity.

If these asset sales are excluded, total losses across the league would exceed £1 billion for the year, the highest on record. These losses must be funded, and an additional £1.3 billion of new finance was raised by clubs, primarily to cover operating shortfalls as well as investment in assets such as Everton’s new stadium.

Net Assets

Net assets represent the difference between total assets and total liabilities and correspond to the club’s net equity.

Assets include fixed assets—such as player registrations, facilities, and goodwill—as well as current assets like trade debtors, transfer fees receivable, and cash.

Liabilities comprise loans (from banks, shareholders, or group companies), transfer fees payable, trade creditors, deferred income (for example, advance season ticket sales), and other financial provisions.

The Friedkin Group’s takeover brought significant changes to the club’s balance sheet. Shortly before the transaction, a £450 million shareholder loan from former owner Farhad Moshiri was converted into equity, effectively removing this liability. In addition, the new owners injected £233 million through a share issue, with the proceeds used to repay a high-cost third-party loan. Together, these steps materially strengthened the club’s net asset position.

At the end of the 2024/25 season, total assets stood at £1.1 billion. This included £813 million relating to the new stadium, £97 million in player assets, and £172 million in other assets, including cash.

These assets were offset by total liabilities of £691 million, comprising £469 million in debt, £65 million in transfer fees payable, and £156 million in other liabilities and provisions.

The table below shows the latest available net asset positions of Premier League clubs, with Everton's net assets of £393 million one of the highest in the division.

There are several balance sheet–related measures within the Premier League’s new financial regulations, which come into effect next year. These fall under the Sustainability and Systemic Resilience (SSR) framework and include:

Working Capital Test

This assesses a club’s immediately available cash headroom over the course of a season. Clubs must maintain at least £12.5 million in short-term liquid assets.

Liquidity Test

This examines medium-term resilience and a club’s ability to withstand financial shocks, such as relegation. A club must demonstrate that its liquid assets, less liquid liabilities, plus 40% of squad market value, exceed £85 million. In practical terms, this reflects whether a club could cover short-term obligations by selling part of its squad if required.

Positive Equity Test

This measures long-term financial health. It includes the full squad market value (or net book value, if higher) as an adjusted asset. Total liabilities must not exceed 90% of adjusted assets, tightening to 80% by 2028/29.

Everton appear well positioned under these tests following the reduction in debt and large asset base. For example, their estimated Positive Equity Test ratio stands at around 53% (see calculation below).

The club reports total assets of £1.1 billion. Based on Transfermarkt estimates, the squad’s market value of £308 million is £211 million higher than its book value, resulting in adjusted assets of approximately £1.3 billion. With total liabilities of £690 million, this equates to 53% of adjusted assets — comfortably within Premier League limits.

Player Trading

Where the impact of Everton’s previous financial difficulties is most evident is in player recruitment. Over the past three seasons, the club has spent £199 million on transfers—the lowest in the division aside from promoted (and subsequently relegated) sides. Over the same period, they generated £180 million from player sales, resulting in a net spend of just £18 million, again the lowest in the league by a considerable margin.

In 2024/25, Everton invested £52 million in new signings, including Jake O’Brien from Olympique Lyon, Iliman Ndiaye from Olympique Marseille, and Carlos Alcaraz from Flamengo.

This outlay was offset by £56 million in player sales, driven primarily by the departure of Amadou Onana to Aston Villa.

As mentioned, Everton’s player spending over the past three years, along with their net trading position, is among the lowest in the league, ahead of only relegated clubs.

There has been a notable shift this season, with the club spending £114 million on players and no major departures. New signings include Tyler Dibling, Thierno Barry, and Kiernan Dewsbury-Hall, all acquired for significant fees. However, it is worth noting that a £114 million spend in a single season still remains below the league average.

Squad Cost and Net Book Value

Squad costs represent the total acquisition cost of all squad members, including transfer fees and associated costs such as agent fees. A squad’s Net Book Value (NBV) represents this acquisition cost less accumulated amortisation, with transfer fees expensed over the length of each player’s contract. For example, a player purchased for £50 million on a five-year contract would have an NBV that decreases by £10 million each year.

As a result of Everton’s constrained spending on players, their net book value has declined in each of the past seven years, falling to £97 million in 2024/25. However, this is expected to increase in the current season following approximately £100 million of investment in the summer transfer window.

Everton's net book value of £97 million is one of the lowest, ahead of only relegated Ipswich.

Squad Market Value

The squad's net book value (NBV) is part of the club balance sheet, recorded as Intangible Player Assets. The NBV does not however reflect a squad’s current market value.

According to Transfermarkt,com Everton’s squad had an estimated market value of around £308 million at the end of the 2024/25 season, placing it among the lower valuations in the division. However, this figure is £211 million higher than the club’s net book value, highlighting both how well players have retained or increased their value and the potential to generate profits through future sales. This £211 million “uplift” ranks as the 11th highest in the league.

Among the most valuable players at that point were Jarrad Branthwaite at £43 million (signed for just £1 million), Vitalii Mykolenko at £24 million, and Dwight McNeil at £22 million.

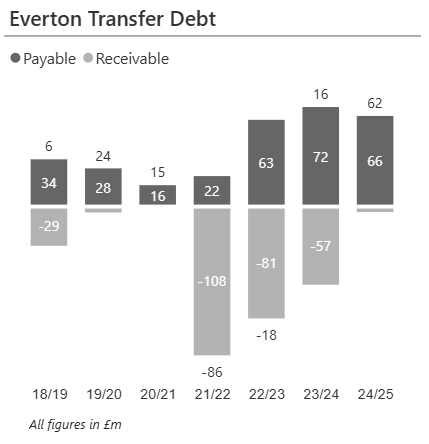

Football Net Debt

As part of the takeover, there was a significant restructuring of the club’s debt.

First, the £450.8 million interest-free shareholder loan provided by Bluesky Capital Limited (the previous owner’s company) was converted into equity, effectively eliminating this liability.

Second, the new owners injected £233 million via a share issue, with the proceeds used to repay a high-cost third-party loan.

Third, a new £350 million loan was secured to refinance existing high-cost borrowings. This facility is repayable over 30 years, with a final maturity date of 30 June 2055. It is secured against the stadium assets and carries interest at market rates.

Fourth, the club put in place a £130 million five-year revolving credit facility with JP Morgan Chase to support working capital requirements.

As a result of this comprehensive refinancing, total debt has reduced from over £1 billion to £469 million. While still substantial, this level of debt is more manageable given the club’s £800 million investment in the new stadium.

Premier League clubs’ total debt is expected to reach £3.3 billion, representing a slight decrease from the previous year.

In 2023/24, Everton recorded the highest overall debt at over £1 billion; however, this has since reduced to £389 million (net of cash), which is likely the third highest in the division, behind only Tottenham (driven by stadium financing) and Manchester United (following their highly leveraged Glazer-era ownership structure).

Following Everton’s recent transfer activity, the club had £66 million owed to other clubs at the end of 2024/25. Transfer fees receivable totalled just £4 million, suggesting that the sale of Amadou Onana was largely settled upfront.

Cash Flow

Cash Flows are reported in three categories:

Cash Flows from Operations refer to cash generated from the club’s core activities—revenue minus day-to-day costs such as salaries, rent, and utilities.

Cash Flows from Investments include cash spent on player acquisitions and facility improvements, net of player or asset sales.

Cash Flows from Financing cover new loans or equity raised, less repayments or buybacks. If operational cash flow cannot fund investments, the shortfall is usually met through financing.

In recent seasons, managing persistent operating losses while simultaneously funding a new stadium placed enormous pressure on the club’s cash flow and, as has been widely documented, brought it close to administration.

The scale of this challenge is evident when examining cash flows over the past five years. Due to high operating costs, the club consumed £186 million in operating cash flow before accounting for any investing activities. Investment in the squad totalled £376 million, although this was largely offset by £342 million generated from player sales.

The stadium project required £771 million of expenditure over the same period, resulting in a combined funding gap of close to £1 billion. To bridge this shortfall, £399 million was raised through share issues and £616 million through loans.

Overall, it was a high-risk strategy, undertaking such a significant infrastructure project while operating from a position of sustained operating losses.

Reporting Entity

This analysis is based on the entity Everton Football Club Company Limited for the period 1st July 2024 to 30th June 2025. The company is owned 99.5% by Roundhouse Capital Holdings Limited. which is 100% owned by Toffee Investments LLC, which is a US-based investment entity that is part of the Friedkin Group, the consortium that acquired Everton.

Comments